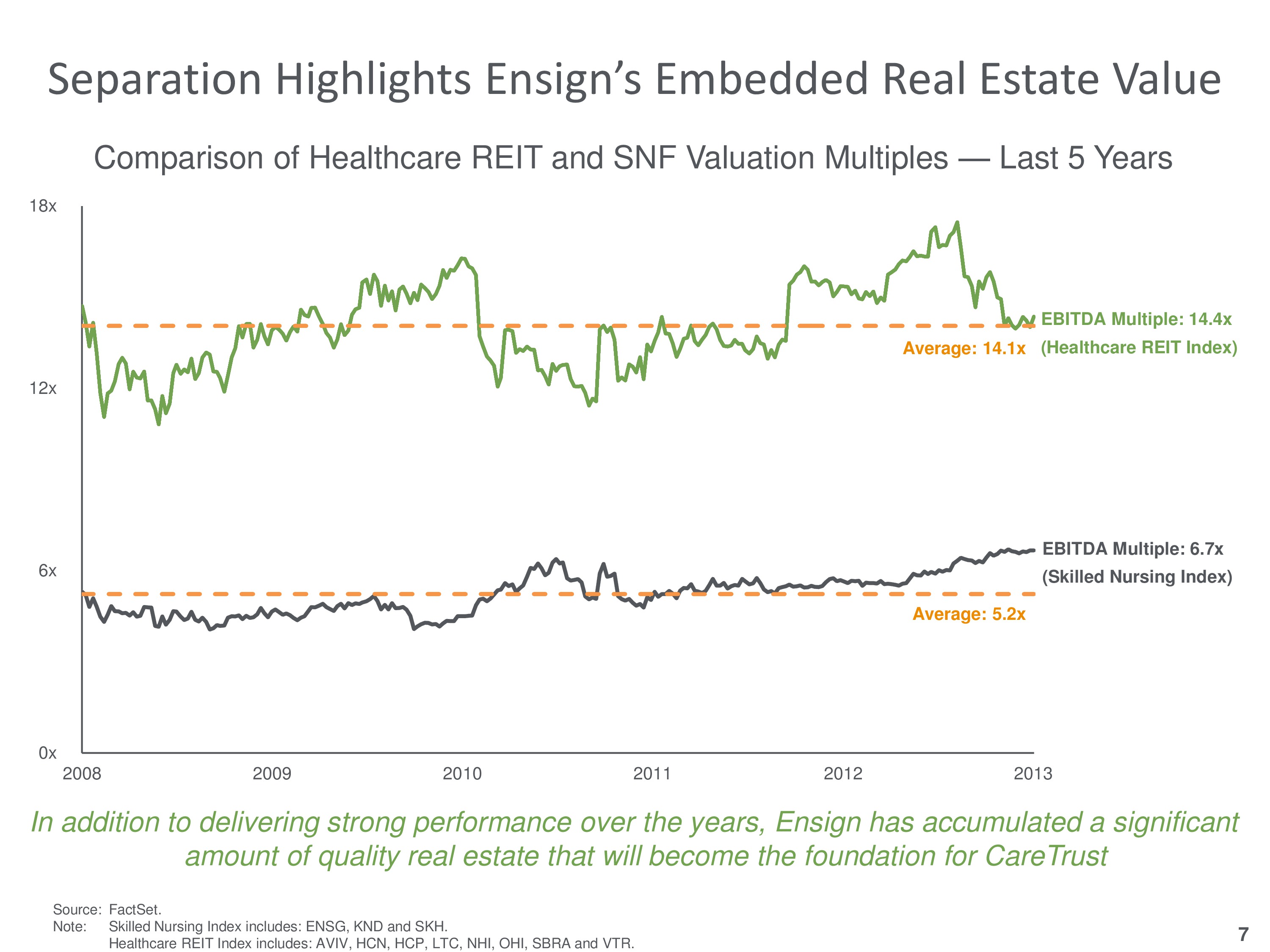

CareTrust will own almost all of the real estate held by Ensign or about 97 facilities as of this November presentation. These properties are expected to generate about $57m in annual rent, with almost all of it coming from Ensign. Although it plans on eventually diversifying its tenant base, there is some risk being solely reliant on Ensign. Sabra Healthcare REIT (SBRA) faced similar issues when it was spun out of Sun Healthcare a few years ago. The presentation and the Form 10 list a bunch of reasons for the spin – access to capital, investor focus, blah blah – but I think Slide 7 does a nice job of summing it up:

Unlocking value by aiming for that nice, fat 14.4x EBITDA Healthcare REIT multiple. CareTrust’s facilities are mostly located in the Western US and a few middle states, but the company expects to expand its geographical base post spinoff as it will no longer be tied to areas where Ensign has a strategic focus. Ensign’s Co-founder and EVP Gregory Stapley (he also holds four other titles) will become CareTrust’s CEO. As part of its newfound REIT status, the company will be forced to pay out a special dividend or ‘purging distribution’ at the end of the year of its allocated earnings and profit.

Ensign will continue offering healthcare services such as skilled nursing and will not be precluded from acquiring new facilities. Ensign’s CEO, Chris Christensen, and CFO, Suzanne Snapper, will remain with the company post-spin. ENSG shares initially reacted positively to the spinoff news, but they have since come back a bit after some recent earnings misses. Although it has faced some challenges, Sabra has performed well since its spinoff, but it’s worth remembering that a) so has the entire market and b) the environment for REITs and the healthcare industry was very different back then.

Disclosure: Author holds no position in any stock mentioned.